Vietnam Tax System - Overview / Cheatsheet (2026)

Know the system or get bullied by it.

1. Overall positioning

Vietnam’s tax system is relatively standard and not aggressive compared to many jurisdictions.

Clear structure

Predictable headline rates

Incentives exist

Compliance = paperwork-heavy rather than conceptually complex

2. Core Taxes

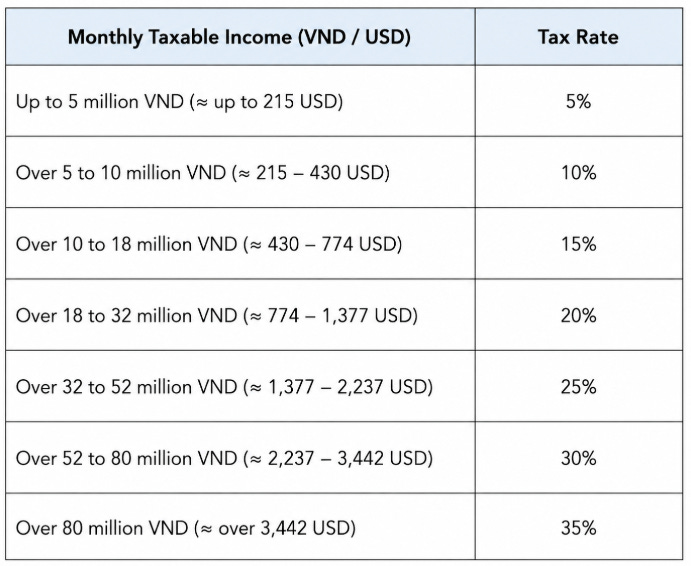

Personal Income Tax (PIT)

Applies to all individuals working in Vietnam (including foreigners)

Tax treatment depends on tax residency status

Resident (≥183 days in Vietnam, or have permanent residence / ≥183 days lease)

Taxed on worldwide employment income

Progressive rates: 0% - 35%

Non-resident

Flat 20% on Vietnam-sourced income

Taxable income

Covers broad categories of income, including:

Salaries and wages

Business income

Capital gains, property, royalties, etc.

For employment income:

Includes salary, allowances, bonuses, benefits

Key deductions

Personal deduction: VND 15.5 million/month

Dependent deduction: VND 6.2 million/month per dependent

Compliance & filing

Employers typically withhold PIT monthly/quarterly

Annual finalisation required:

By employer or individual depending on situation

Deadlines:

~March (employer) / April (individual) after year-end

Practical takeaway: Vietnam PIT is residency-based: residents pay progressive tax (up to 35%) on worldwide income, while non-residents pay a flat 20% on Vietnam-sourced income. The actual tax depends heavily on deductions and proper classification of income/benefits. Employers typically handle withholding, but annual finalisation is still required.

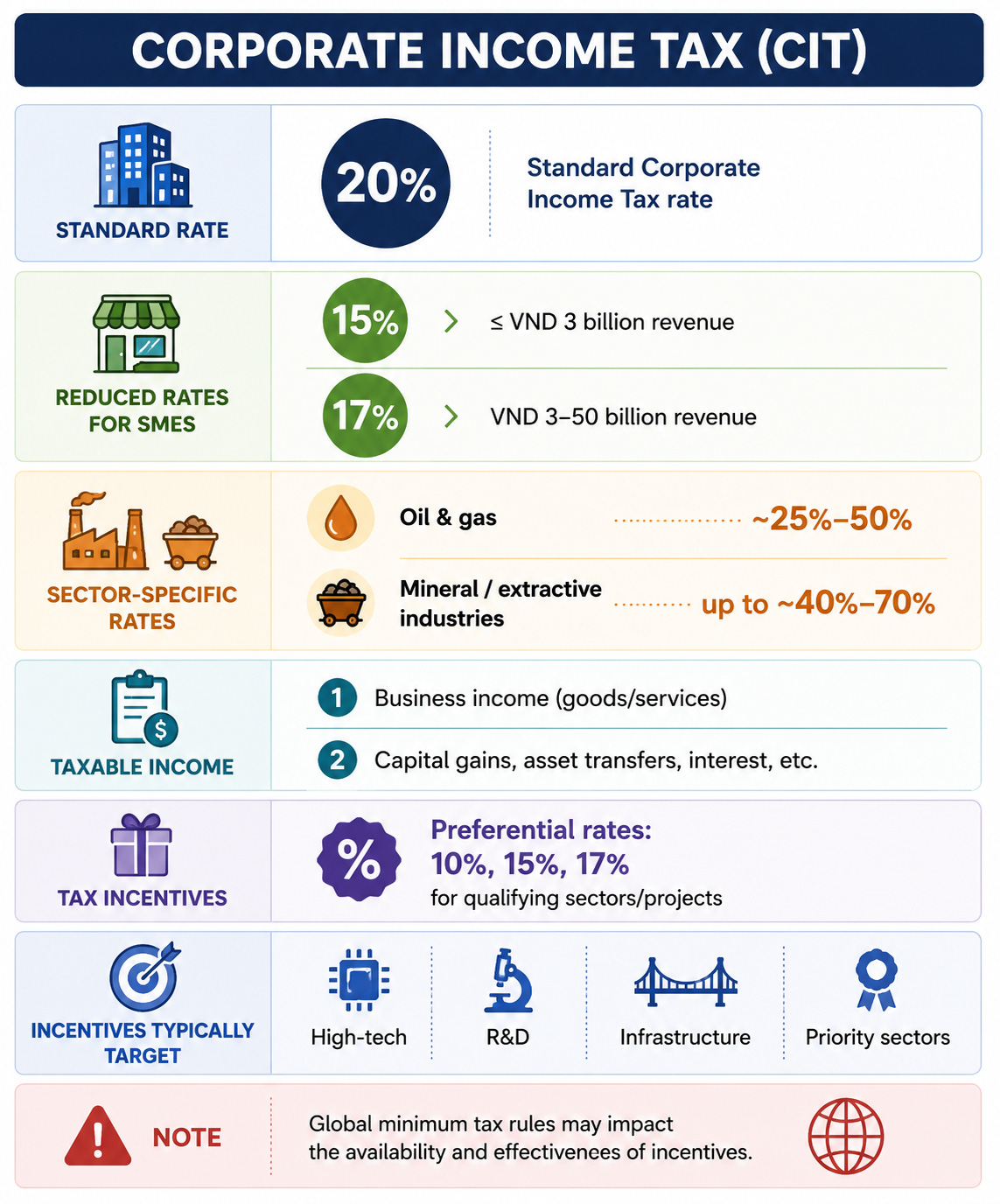

Corporate Income Tax (CIT)

Scope

All enterprises operating in Vietnam (local and foreign)

No tax residency concept for CIT

Companies established in Vietnam are taxed on worldwide income

Standard rate: 20%

Reduced rates for SMEs:

15% (≤ VND 3 billion revenue)

17% (VND 3–50 billion revenue)

Sector-specific rates

Oil & gas: ~25%–50%

Mineral / extractive industries: up to ~40%–70%

Taxable income

Business income (goods/services)

Capital gains, asset transfers, interest, etc.

Calculation: Revenue – deductible expenses + other income

Key deductions & losses

Expenses must:

Be business-related

Be properly documented

Loss carryforward:

Up to 5 years

No carryback allowed

Tax incentives

Preferential rates: 10%, 15%, 17% for qualifying sectors/projects

Note: global minimum tax rules may impact this (see below)

Incentives typically target:

High-tech, R&D, infrastructure, priority sectors

May include:

Tax holidays (exemption periods)

Reduced rates for a period

Foreign companies / cross-border

Foreign companies without entity in Vietnam:

Subject to Foreign Contractor Tax (FCT) (see below)

With permanent establishment:

Taxed on Vietnam + related foreign income

Compliance & filing

Quarterly provisional CIT payments required

Annual finalisation:

Due ~3 months after year-end

New development: Global Minimum Tax

Vietnam adopts 15% Global Minimum Tax (from 1 Jan 2024) under OECD rules

Applies to large MNCs (> €750M global revenue)

Mechanism (adopted OECD Pillar Two rules):

Either:

Vietnam collects (QDMTT - “Qualified Domestic Minimum Top-Up Tax“)

OR HQ country collects (IIR - “Income Inclusion Rule“)

Practical takeaway: Vietnam’s CIT is straightforward: most companies pay ~20%, with lower rates or incentives only if specific conditions are met. The real outcome depends on how you structure your presence (local entity vs FCT) and how well expenses are documented. For large MNCs, global minimum tax rules (15%) may limit the benefit of local incentives.

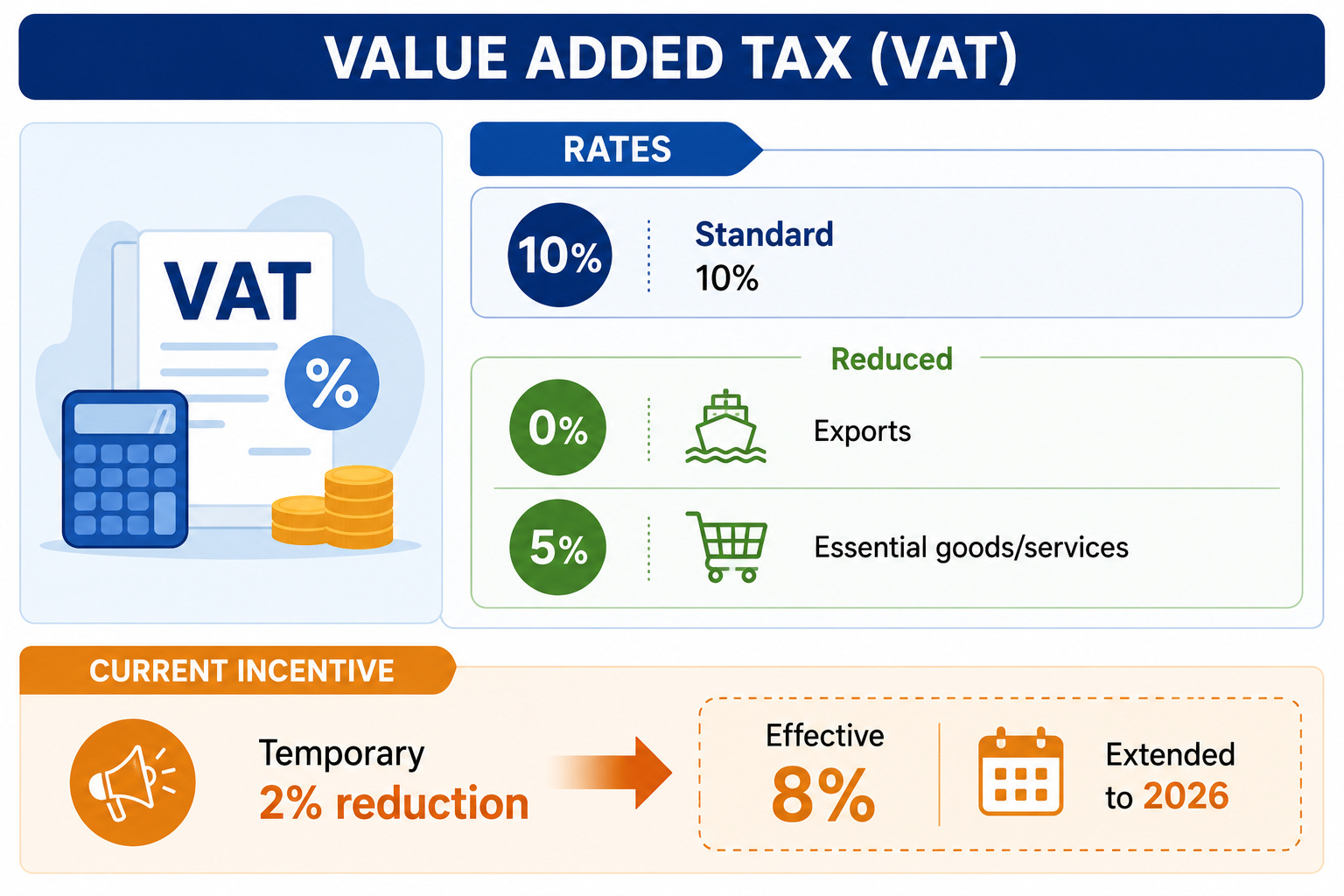

Value-Added Tax (VAT)

Nature

Indirect consumption tax applied on goods & services in Vietnam

Applies to most domestic transactions + imports

Charged at each stage of production/distribution, ultimately borne by final consumer

Scope

Goods & services used for production, trading, consumption in Vietnam

Includes imports + foreign-sourced services

Imports → VAT paid at customs together with import duties

Rates

Standard: 10%

Reduced:

0% → exports

5% → essential goods/services

Current incentive:

Temporary 2% reduction → effective 8%, extended to 2026

Calculation methods

Deduction Method (main method)

Formula: VAT payable = Output VAT – Input VAT

Key points: Used by most companies (esp. FIEs)

Requires:

Proper accounting records

Valid VAT invoices

Input VAT credit allowed if compliant

Direct Method

Used for:

Small businesses / individuals

Non-compliant accounting cases

Rates applied on revenue:

Goods trading: 1%

Services: 5%

Production/transport: 3%

Other: 2%

E-commerce/platforms: 10%

Exemptions

Examples:

Financial services

Securities

Insurance (certain)

Land use rights transfer

FX services

No declaration / no payment

Certain agricultural raw products resold

Still can deduct input VAT

Export VAT (0%)

Applies if:

Goods/services consumed outside Vietnam

Proper supporting documents provided

Filing & Payment

Based on turnover:

VND 50B → Monthly filing

≤ VND 50B → Monthly or quarterly

Deadlines:

Monthly → 20th of next month

Quarterly → End of next month after quarter

Refunds

Eligible cases:

Exporters with ≥VND 300M input VAT credits

Investment projects (pre-operation phase)

Businesses mainly taxed at 5%

ODA (Official Development Assistance) / special cases

Key limits:

Export refund capped at 10% of export revenue

Carry forward:

Excess input VAT → carried to next period

E-Invoicing (mandatory)

Required since 1 July 2022

Must register with tax authority before use

Practical takeaway: Vietnam’s VAT system is standard, broad-based, and predictable. It works mainly by offsetting input VAT against output VAT. The temporary reduction from 10% to 8% (to 2026 for certain items) is a key commercial point, while VAT refunds can be meaningful for exporters and investors. Compliance depends heavily on proper invoices, documentation, and choosing the correct method.

3. Special / Industry Taxes

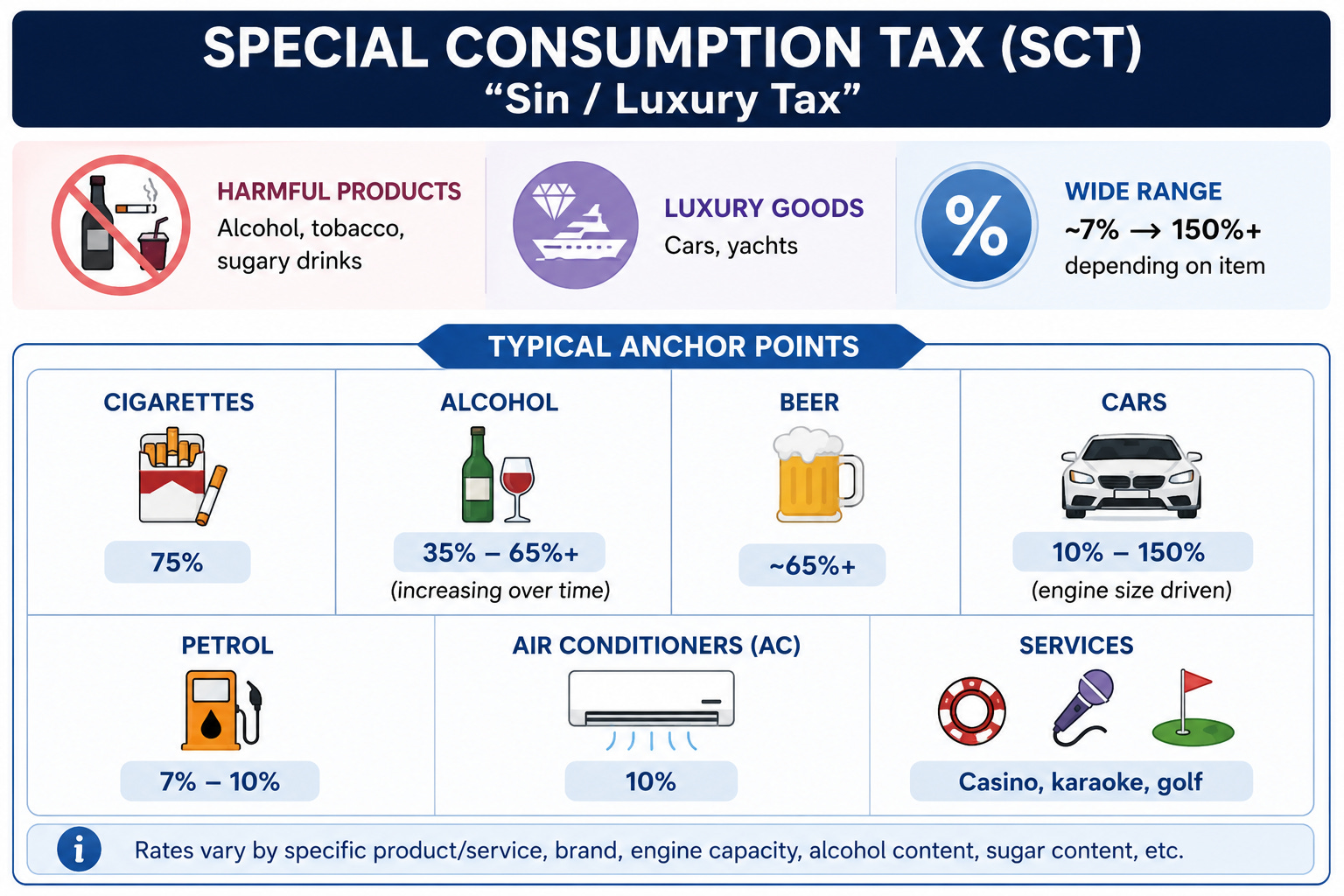

Special Consumption Tax (SCT) - “Sin / Luxury Tax”

Targets:

Harmful products (alcohol, tobacco, sugary drinks)

Luxury goods (cars, yachts)

Services (casino, karaoke, golf)

From 2026 onwards — tightening significantly:

Key changes:

Dual structure:

% of price

+ fixed tax per unit (new)

Expansion:

Broader coverage across goods (11 categories) & services (6 categories) - key ones:

Tobacco (cigarettes, cigars)

Alcohol (spirits, wine, beer)

Cars (<24 seats)

Motorbikes (>125cc)

Petrol

Air-conditioners

Luxury items (yachts, airplanes)

Playing cards / votive paper

Nightclubs / discos

Karaoke / massage

Casinos / gaming

Betting

Golf

Lotteries

NEW trend: sugary drinks (from 2027)

Trend:

Rates increasing over time (not one-off)

Alcohol/beer → up to ~90%

Tobacco → rising + per-pack tax

Cars → higher rates for bigger engines

Who pays

Producers

Importers

Service providers

Wide range: ~7% → 150%+ depending on item

Typical anchor points:

Cigarettes: 75%

Alcohol: 35% – 65%+ (increasing over time)

Beer: ~65%+

Cars: 10% – 150% (engine size driven)

Petrol: 7% – 10%

AC: 10%

Offset against double tax:

Raw materials already taxed; and/or

Impact → sell locally

Practical takeaway: 1) SCT rates are high + increasing as general trend; 2) Policy-driven → expect ongoing changes

Foreign Contractor Tax (FCT)

Applies when foreign companies earn Vietnam-related income without a local entity.

Structure:

Combination of:

VAT + income tax (CIT/PIT)

Typical effective rate: ~5–10%

Filing timeline: ~10 days

Very broad scope (no physical presence needed):

Services in Vietnam (consulting, marketing, SaaS, training, etc.)

Services partly performance / linked to Vietnam (installation, maintenance)

Online services (ads, SaaS, training, platforms etc)

Bundled goods + services

Royalties, interest, commissions, licensing

Not applicable:

Pure goods import (no services)

Services fully performed & consumed outside Vietnam

Mechanism:

Vietnamese party withholds tax before payment (within 10 days of payment)

Pays to government on behalf of foreign contractor

Practical takeaway: FCT broadly applies to most cross-border payments from Vietnam (even without a local entity), so always factor ~5–10% tax into pricing upfront. The Vietnamese party must withhold and pay within ~10 days, and poor contract structuring can lead to higher tax exposure.

Import / Export Duties (Customs Tax)

Import tax: varies by product - multiple tax layers (not just tariff)

Import duty

VAT (typically 10%)

SCT (if applicable - e.g. alcohol, cars)

Anti-dumping / safeguard duties (if applicable)

Export tax: limited, many exemptions

Mostly 0% duty

Applies mainly to natural resources (minerals, etc.)

What drives the tax rate

3 key factors:

HS code (classification) → determines base rate

Origin of goods → MFN (standard) vs Preferential (WTO) vs FTA (ASEAN) rates

Type of goods → consumer (higher) vs machinery (lower)

MFN rates (Most Favoured Nation)

Default import tax rate

Applies if:

No special trade agreement applies, or

You can’t prove origin

Usually higher than FTA rates

FTA rates (Free Trade Agreement)

Preferential (lower, sometimes 0%) tax rate

Applies if:

Goods come from an FTA partner country (e.g. China, Korea, EU, ASEAN, CPTPP countries), and

You meet rules of origin + have proper documents (e.g. Certificate of Origin – CO)

Timing

Import: before clearance

Export: within ~30 days

Practical takeaway: Import duties in Vietnam are mainly driven by HS code classification and origin (FTA vs non-FTA), so getting these right upfront is the biggest cost lever. Duties (plus VAT/SCT if applicable) must be paid before clearance, meaning mistakes directly impact cash flow and shipment delays.

4. Other Relevant Taxes

Natural resources tax

Environmental tax

Land use tax (manufacturing, energy, real estate)

5. Business License Tax (BLT)

Nature: annual registration fee ranging from VND 1 million to 3 million based on charter capital or revenue, typically paid at the start of each year

Eliminated from 1 Jan 2026

6. Key Takeaways

System is standard → complexity is in paperwork, not rules

PIT = residency-driven → global vs VN-only tax changes everything

CIT ≈ 20% baseline → incentives exist but not automatic

VAT = input vs output → 8% (temp) is key commercial lever

FCT hits most cross-border flows → assume ~5–10% tax leakage

Customs = HS code + origin → biggest driver of cost (FTA can → 0%)

SCT = high & rising → policy-driven (sin/luxury sectors)

Execution matters most → structure, docs, classification = real outcome